Social VR platform Rec Room, once valued at $3.5 billion, announced earlier this week that it will be shutting down in June. The studio says it never quite figured out how to turn a profit, though top avatar creator blueasis maintains the story is a bit more complicated.

If you’ve ever seen the weird little VRChat avatar ‘Brush the Marmoset’—a staple of Internet memes since 2020—you’re likely already familiar with blueasis.

While they’re one of the OG 3D character and environment artist on VRChat, they’re also the top creator on Rec Room, which gives them a fair bit of insight into why the platform’s decade-long existence is soon coming to an end.

As one of the most well-funded VR companies to date, the Seattle-based studio attracted over $294 million since its founding in 2016. Its most recent round came in December 2021, bringing to the company $145 million and briefly giving it a $3.5 billion valuation.

Despite its popularity and enviable startup runway, the company said earlier this week it “never quite figured out how to make Rec Room a sustainably profitable business. Our costs always ended up overwhelming the revenue we brought in. We spent a long time trying to find a way to make the numbers work.”

In a thread on X, blueasis gives an insider perspective on why they think Rec Room is closing up shop. In short, it wasn’t a bad creator economy or lack of returning users; the company just sort of … bungled things.

“I joined Rec Room 1.5 years ago to participate in their avatar cosmetics program,” blueasis recounts. “I made lots of items (2000~) honed my craft, became the number 1 seller on the entire platform, met awesome creatives & talked directly with the team.”

“My estimation of the shutdown; overhiring during the covid boom, making promises they couldn’t keep, continually gambling on new players & tech before focusing on the core experience & existing players.”

Having joined in late 2024, blueasis says it was “immediately obvious that the community was unhappy.”

“Spending so much money on player acquisition, mobile, console etc, with little to no payoff, these users rarely became creators, rarely spent money on the platform etc. The people who cared about the platform, PC, VR, did! but they were neglected in favor of ‘growth’.”

It was ostensibly that gamble to push for rapid expansion that ultimately tipped the studio into its first big tailspin: in August 2025 the company laid off around half of its staff, citing costs related to a surge in low-level content flooding the platform from users on mobile and console.

“I think by the time they realized this it was too late, the numbers were already dire, so they had to keep trucking along in any direction that would make them revenue, which just meant more gambling new features to hope something stuck, AI pet chat bot was a big one people hated.”

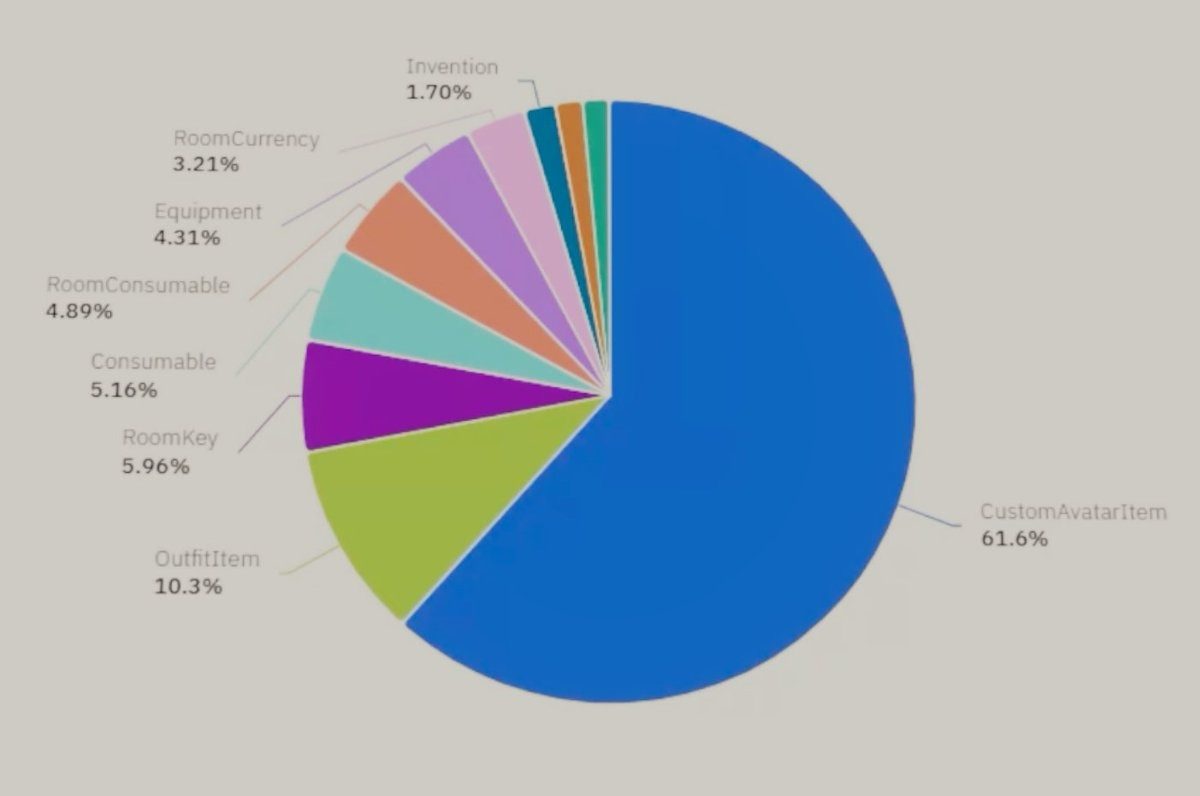

Blueasis says the platform’s push for user-generated avatar cosmetics was “their biggest success,” which they reveal accounted for 60% of player spend, “outselling Rec Room original items by 10x.”

In September 2025—notably just one month after laying off half its staff—the company announced it was paying out more than a million dollars per quarter to creators. That’s a lot of money coming in, a lot leaving into the hands of creators, and surprisingly little captured by the company.

Blueasis highlights the popularity of the UGC avatar cosmetics program and its outsized share of player spend, although the platform’s modest rake on creator sales may also be a big contributing factor.

While the company retains 70 percent revenue after paying platform fees on first-party content, when it comes to UGC, Rec Room only takes a 30 percent rake. This leaves creators with the bulk of the revenue, meaning Rec Room retained far less from top-selling items.

In the end, low fees are usually a powerful tool to help acquire an initial userbase. But they aren’t a lasting strategy, especially when new users aren’t contributing to the ecosystem in a way that offsets costs. And it seems the studio got interminably stuck in that dangerous gap between aggressive user acquisition and eventual platform stability—and just never managed to climb out.